With the advent of 2015, there is a change of our Malaysia’s main reference rate. It has been changed from Base Lending Rate (BLR) to Base Rate (BR) effective 2nd January 2015. The aim of the current BR is to promote better transparency, pricing discipline and efficiency among financial institutions.

Here is the the official release from Bank Negara Malaysia (BNM):-

https://docs.google.com/file/d/0BxFNt13XnYKuZFp3M1hkVHJNaTQ/view?pli=1

How does the new Base Rate affects you?

Loan taken BEFORE 2nd January 2015:–

Existing loans that currently pegged to BLR/BFR will continue as it is, until full loan or financing settlement or up to a renewal or refinancing. So you might want to consider refinancing by using the new Base Rate if it is lower. This means the BR does not affect you unless you take up a new loan or go for refinancing.

Loan taken AFTER 2nd January 2015:–

Loan for financing taken after 2 January 2015 will certainly be based on Base Rate. The good news is, with the current system, you can now compare and choose the best lending rate for your new loan as different financial institutions will have different base rate.**source from BNM, for the full table, you may download here (Click Here:- http://www.bnm.gov.my/documents/2015/base_rates/20150102_base_rates.pdf )**

The new framework is expected to provide transparency to the financial institutions’ efficiency and performance compared to the old BLR framework. This is because the new Base Rate will differ from one financial institution to the other. This will then mean the market will be more competitive by offering more attractive financing packages.

Nonetheless, when it comes to the Calculation of Effective Lending Rate, kindly take note that financial institutions are given the flexibility to determine their respective benchmark rates, and this in turn might increase or decrease in your repayment if there is any change in the Base Rate. It is prudent for you to check with your solicitors or bankers before you decide on which loan package to take before you sign on to one.

The implementation of the BR should be a good thing as the new Base Rate would be partially determined by the efficiency of financial institutions.

Here is the official press statement by BNM:-

New Reference Rate Framework

Bank Negara Malaysia announces today that effective 2 Jan 2015, the Base Rate will replace the Base Lending Rate (BLR) as the main reference rate for new retail floating rate loans.

Since the introduction of the BLR framework in 1983, the BLR has served as the main reference rate on retail floating rate loans in Malaysia. Since then, the determination and implementation of the BLR has evolved with the development of the financial sector. In the recent period, however, the BLR has become less relevant as a reference rate for loan pricing, as lending rates on new retail loans are being offered at substantial discounts to the BLR. The BLR also lacks transparency, which makes it difficult for consumers to make an informed decision.

The new Reference Rate Framework aims to provide a more transparent reference rate to enable better decision by consumers in making choices among the many loan products offered by financial institutions. The new reference rate will also better reflect changes in cost arising from monetary policy and market funding conditions, while encouraging greater discipline and efficiency among financial institutions in the pricing of retail financing products.

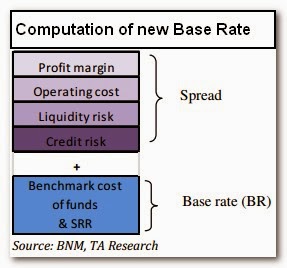

The Base Rate will be determined by the financial institutions’ benchmark cost of funds and the Statutory Reserve Requirement (SRR). Other components of loan pricing such as borrower credit risk, liquidity risk premium, operating costs and profit margin will be reflected in a spread above the Base Rate. This increases the visibility of the factors underlying changes to the Base Rate. The greater transparency in turn will enable more informed decision making by consumers. Under this cost-plus structure, spreads will always be positive as it would not be possible for financial institutions to offer lending rates below the reference rate. Financial institutions will be given the flexibility to determine their respective benchmark rates. The expected strong link between the Base Rate, market interest rates and the Overnight Policy Rate (OPR) will facilitate more complete adjustments to retail loan repayments when market interest rates adjust to an increase or decrease in the OPR.

The Base Rate will be used for new retail floating rate loans and the refinancing of existing loans extended from 2 January 2015 onwards. After the effective date, BLR-based loans prior to 2015 will continue to be referenced against the BLR. However, when a financial institution makes any adjustments to the Base Rate, a corresponding adjustment to the BLR will also be made. As such, financial institutions would be required to display both their Base Rate and BLR at all branches and websites.

The shift to the new Reference Rate Framework should have no impact on the effective lending rates charged to retail borrowers which are determined by various factors, including a financial institution’s assessment of a borrower’s credit standing, market funding rates and competitive considerations. It is also important to note that the changes do not represent a change in the Bank’s monetary policy stance.

Bank Negara Malaysia

19 March 2014